Introduction to GST and the Importance of Case Laws

The Goods and Services Tax (GST) is a significant achievement in the realm of tax reform in India, implemented with the objective of creating a unified tax structure that simplifies indirect taxation. Enacted on July 1, 2017, GST combines various indirect taxes, such as the central excise duty, service tax, and Value Added Tax (VAT), into a single comprehensive tax system that is levied on goods and services. This transition to a streamlined tax structure is aimed at enhancing tax compliance and reducing the complexity involved in tax collection.

GST operates on a dual model, where both the Central and State governments impose taxes on the same transaction, ensuring that tax revenue is shared between them. The key features of GST include the input tax credit mechanism, a definite tax rate framework, and a self-assessment principle, among others. By facilitating seamless credit availability across the supply chain, GST has contributed to a significant decrease in the overall tax burden on goods and services, thereby fostering a more conducive environment for business operations.

Case laws play a crucial role in the interpretation and implementation of GST provisions. As tax professionals and businesses navigate the intricate maze of GST regulations, judicial precedents help clarify ambiguous provisions, guiding stakeholders in their compliance efforts. These case laws serve as legal references for understanding the applicability of GST in various scenarios and resolving disputes that may arise during assessments. Moreover, they contribute to a more predictable regulatory environment, reinforcing taxpayers’ confidence in the system.

In essence, staying updated with the latest GST case laws is vital for tax professionals, businesses, and legal practitioners. Understanding how courts interpret GST provisions provides valuable insights into evolving tax practices, ensuring that all parties involved are well-equipped to respond to any challenges posed by the tax framework.

The case of Jawandamal Dhanamal vs Union of India arises within the complex landscape of Goods and Services Tax (GST) legislation, which has undergone significant scrutiny and reform since its implementation. The parties involved include Jawandamal Dhanamal, a dealer registered under the GST regime, and the Union of India, representing the goods and services tax authorities responsible for compliance enforcement. The core legal context revolves around the issuance of a Show Cause Notice (SCN) and the classification of transactions under the GST framework.

The heart of the issue lies in whether the SCN issued against Jawandamal accurately reflects the essence of the transaction and complies with the principles established under GST regulations. There were several allegations concerning the underreporting of tax liabilities and improper classification of goods, which prompted the legal dispute. The aim was to clarify the procedural legitimacy and substantive merit of the SCN in light of existing laws, thus affecting the dealer’s operational standing and compliance obligations.

A timeline of events leading to the court’s hearing reveals a series of proceedings that escalated from initial notices to multiple layers of appeals. Jawandamal contended that the SCN submitted lacked adequate grounds and failed to meet the requirements of providing a clear rationale for the tax liabilities stated. This culminated in a formal legal challenge, hoping to set a precedent regarding the adequacy of SCNs in GST enforcement. The implications of this case extend beyond the immediate parties involved, having a broader significance in shaping GST enforcement and compliance practices across India.

Given the evolving nature of GST legislation, cases like Jawandamal Dhanamal vs Union of India serve as a crucial reference point for understanding the interpretations and operational challenges within the GST framework today.

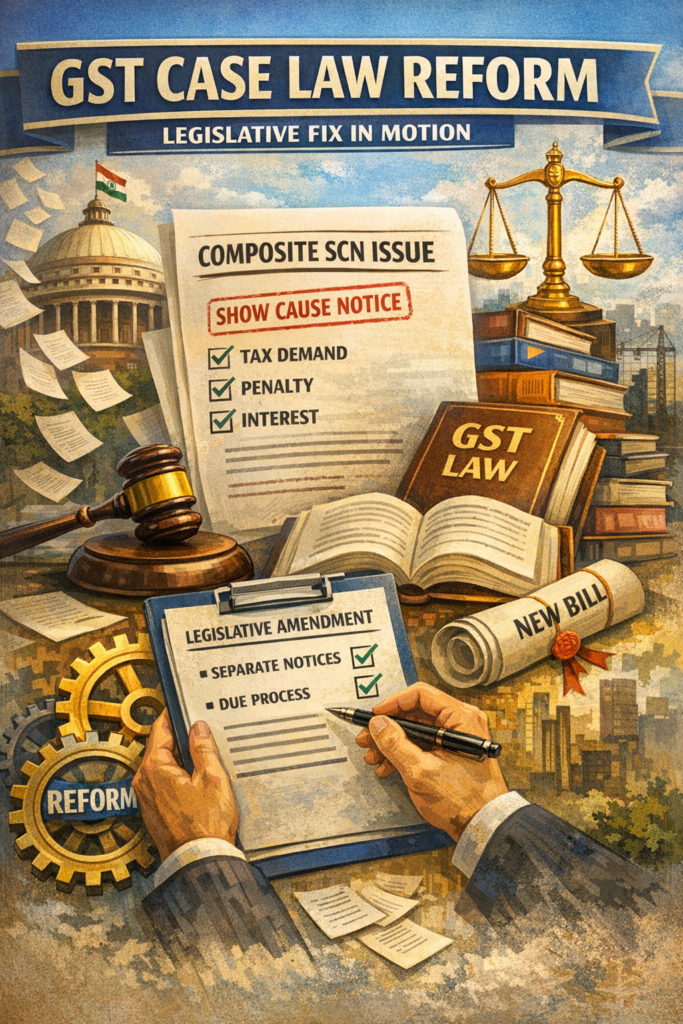

Composite Show Cause Notice (SCN) Issues Explained

A Composite Show Cause Notice (SCN) is an instrument within the Goods and Services Tax (GST) framework utilized by tax authorities to inform taxpayers about non-compliance or irregularities concerning tax matters. These notices typically outline the reasons for the allegations, provide evidence of purported violations, and establish a framework for the taxpayer to respond. The SCN is essential in ensuring procedural fairness and compliance, ensuring that taxpayers have a chance to present their defenses before any adverse actions are taken against them.

The controversies surrounding Composite SCNs primarily center on the complexities involved in compliance and the potential for procedural unfairness. Taxpayers often face challenges regarding the clarity and specificity of the notices received. In some instances, taxpayers have reported that SCNs combine multiple allegations and subjects, which may obfuscate the taxpayer’s understanding of the charges. Such a conflated notification raises concerns about the ability of taxpayers to adequately respond, as it muddles distinct issues that should ideally be addressed separately.

The implications of ambiguous or composite SCNs can be significant, leading to confusion among taxpayers regarding their obligations and the severity of the penalties they might face. Moreover, an inadequately defined notice may hinder taxpayers’ capacity to prepare an informed response, potentially resulting in unfavorable rulings. This has triggered discussions within both the legislative bodies and the tax administration regarding possible reforms to ensure compliance processes are more transparent and equitable.

As the GST landscape evolves, the challenge of effectively managing Composite SCNs remains a critical topic of discussion. Stakeholders are advocating for adjustments in the SCN procedures to streamline issues of clarity and to enhance the overall compliance experience for taxpayers, ensuring that fair and just processes are upheld as part of the GST regime.

In the recent proceedings before the Gujarat High Court, the Additional Solicitor General (ASG) articulated significant arguments addressing the challenges posed by the Composite Show Cause Notice (SCN) in the context of the Goods and Services Tax (GST). The ASG emphasized that the government’s proactive stance towards amending the legislative framework aims to bring clarity and efficiency to the GST compliance landscape. This initiative is driven largely by the need to rectify procedural anomalies arising from the issuance of Composite SCNs.

The essence of the ASG’s submissions revolved around the assertion that current legislative provisions may inadvertently create complexities for taxpayers. The Composite SCNN presents a myriad of challenges, particularly regarding the principles of natural justice. The ASG highlighted that the government’s ongoing legislative efforts are designed to address these issues comprehensively, ensuring that taxpayers are afforded fair opportunities to respond to notices without facing undue hardships.

Moreover, the ASG drew attention to the importance of amicable resolutions between the government and taxpayers. By acknowledging the hurdles associated with the Composite SCN, the government aims to foster a cooperative regulatory environment. This approach is viewed as a crucial step in facilitating compliance and promoting transparency in the administration of GST.

Furthermore, the ASG stressed that the proposed legislative modifications will be thoroughly examined to mitigate potential disputes in the future. The government’s rationale is not solely to rectify past ambiguities but also to prevent future occurrences that may disrupt the orderly functioning of the GST regime. It is anticipated that these legislative amendments will be introduced to the Parliament, potentially transforming how composite tax compliance matters are dealt with under the GST framework.

Analysis of the Gujarat High Court’s Role

The Gujarat High Court has emerged as a pivotal authority in the realm of Goods and Services Tax (GST) disputes, particularly concerning the issue of composite show cause notices (SCNs). As one of the high-ranking judicial bodies in India, it holds significant responsibilities in interpreting GST laws and addressing the complexities that arise from them. With a rise in legal challenges related to GST compliance, the court’s decisions play a critical role in shaping the future of tax administration and legislative amendments.

In recent judgments, the Gujarat High Court has underscored the importance of ensuring that taxpayers receive adequate opportunity to present their case before any punitive action is taken. This highlights the judiciary’s committed stance towards safeguarding taxpayer rights while also ensuring the proper application of GST laws. The court’s interpretations of various GST provisions can lead to substantial changes in how tax authorities approach enforcement actions, thereby influencing not only current case laws but also the potential for future legislative adjustments.

Moreover, the high court’s decisions serve as precedents that can guide lower courts and tax authorities in similar situations. By meticulously dissecting intricate aspects of GST legislation, especially those surrounding composite SCNs, the Gujarat High Court is influencing a more user-friendly tax administration environment. Such an approach not only emphasizes judicial prudence but also reflects an understanding of the commercial realities faced by taxpayers.

Ultimately, the role of the Gujarat High Court in adjudicating GST-related disputes is instrumental in nurturing a balanced relationship between the tax framework and taxpayer interests. The implications of its rulings extend beyond immediate resolutions as they contribute to the evolving landscape of GST jurisprudence in India.

Potential Legislative Fixes and Their Implications

The introduction of legislative fixes aimed at addressing the issues related to Composite Show Cause Notices (SCNs) is a pivotal development in the Goods and Services Tax (GST) ecosystem. These measures are designed to streamline the process and resolve the ambiguities that have arisen in the interpretation and enforcement of existing regulations. One of the key proposals includes the explicit delineation of the parameters that govern the issuance of Composite SCNs, thereby reducing the uncertainties faced by taxpayers and legal practitioners alike.

Furthermore, one of the most significant potential legislative changes is the introduction of clearer guidelines regarding the information requirements in Composite SCNs. This amendment would ensure that taxpayers receive detailed and specific allegations, allowing them to prepare their defense adequately. Such transparency is expected to foster an environment of fairness and clarity, which, in theory, should enhance compliance rates and reduce litigation instances.

Another potential fix could involve adjusting the timelines within which these notices must be responded to, providing taxpayers with a reasonable opportunity to contest the claims. The implications of this change are substantial; extended timelines could lead to reduced pressure on businesses, allowing for better resource allocation towards compliance and dispute resolution.

For legal practitioners, these legislative fixes present an opportunity to adapt their strategies and functioning in response to the evolving GST landscape. They may need to update their legal frameworks, reassess client advisement, and refine their approach in representing clients in GST-related disputes. Overall, these potential changes signify a move towards a more refined GST regulatory framework, aiming to create a balanced approach that accounts for the interests of both the revenue authorities and the taxpayers.

Impact of the Case Ruling on Future GST Disputes

The recent ruling in the Jawandamal Dhanamal case has significant implications for future Goods and Services Tax (GST) disputes, particularly in the interpretation and enforcement of laws surrounding composite show cause notices (SCNs). This landmark decision has the potential to reshape how GST authorities approach the issuance of SCNs and how taxpayers engage with compliance procedures.

Historically, the issuance of composite SCNs in GST matters has been a point of contention, often leading to litigation and appeals. The ruling underscores the necessity for clarity and precision in the issuance of such notices, signaling a judicial preference for a more nuanced understanding of the legal requirements involved. This change could minimize the contentious nature of disputes arising from ambiguous notices and enhance overall tax compliance.

Furthermore, the Jawandamal Dhanamal case may usher in a shift towards a more taxpayer-friendly approach. Legal interpretations may evolve to emphasize the protection of taxpayer rights, thereby reducing the likelihood of arbitrary decisions by GST authorities. As enforcement mechanisms adapt, it is plausible that subsequent cases will reference this ruling as a guiding framework for similar disputes, thereby establishing stronger precedents.

In light of these developments, businesses should remain vigilant and reassess their compliance strategies in response to the evolving legal landscape. Organizations may consider proactively engaging with legal counsel to navigate the implications of this ruling on their operations. Overall, the decision signals a meaningful shift in the adjudication of GST matters, reflecting a growing recognition of fairness in tax administration while also upholding the integrity of the GST framework.

Recommendations for Taxpayers and Practitioners

The ongoing developments regarding the latest GST case laws highlight the necessity for taxpayers and legal practitioners to remain vigilant and informed about potential legislative changes. To navigate the complexities of the GST landscape effectively, several strategic insights can be adopted.

First, it is advisable for taxpayers to keep abreast of the latest updates regarding GST legislation, particularly those that pertain to the composite show cause notice (SCN) issue. Engaging in regular training sessions or subscribing to professional updates can help in understanding the nuances of any evolving laws. Practitioners should encourage their clients to maintain thorough documentation and clear records of all transactions, as this will facilitate compliance and diminish the risks of future disputes.

Moreover, taxpayers should consider conducting periodic audits of their GST filing to identify discrepancies and rectify them proactively. This proactive approach not only aids in compliance but can also bolster the confidence of the taxpayer in managing their GST liabilities effectively. Legal practitioners can assist by using technology solutions that streamline the tracking and analysis of GST-related transactions.

Collaboration with other industry peers can also provide invaluable insights into best practices that can be adopted in light of legislative uncertainties. Taxpayer forums or informal networks can serve as platforms for sharing experiences and strategies regarding GST compliance. Staying involved in discussions surrounding policy changes or attending workshops organized by tax authorities can further enhance understanding.

Lastly, it is prudent for both taxpayers and practitioners to be prepared for potential legal challenges as the GST landscape evolves. Establishing a robust legal strategy in anticipation of such changes will position stakeholders to respond effectively and efficiently, ensuring that they can adapt to new requirements as they arise.

Conclusion and Outlook

The recent developments surrounding the Jawandamal Dhanamal case provide significant insight into the complexities of Goods and Services Tax (GST) regulations in India. As the case illustrates, the issues related to the issuance of a Composite Show Cause Notice (SCN) have prompted a necessary examination of existing legislation. This specific case emphasizes the need for clearer regulatory frameworks to ensure compliance while also safeguarding taxpayer rights.

Additionally, ongoing legislative efforts are noteworthy as they signify a proactive approach by the authorities to rectify ambiguities associated with GST provisions. The existing challenges underline the critical nature of adaptive legislation that not only addresses current discrepancies but also anticipates future developments in the tax landscape. Such responsiveness is vital for maintaining the integrity and efficacy of GST laws, ultimately aimed at fostering a more robust tax regime.

Looking ahead, the implications of the Jawandamal Dhanamal case are likely to reverberate through future GST case laws and rulings. As legal precedents evolve, they will contribute to shaping a more informed and transparent taxation environment, which is essential for both taxpayers and the government. The continual evolution of tax legislation reflects a broader trend of refining administrative processes, thereby enhancing compliance mechanisms.

In conclusion, while the road ahead entails navigating through complexities, the commitment to reform and legislative clarity indicates a promising outlook for GST case laws. Stakeholders must remain informed and engaged in these developments to adapt effectively to the ever-changing tax landscape in India.

Pingback: Banks’ Liability for Third-Party Fraud Under Scrutiny in Landmark Consumer Protection Case – smeaccountant